THE UN-OFFICIAL PENSION NEWSLETTER – JULY 2021

Legal Theft at Our Pension Fund

Over the years, as your pension fund trustee, I have written newsletters in an attempt to counter who I call the City Apologists, those that try to discount or discredit any genuine concern for our pension fund’s integrity. Many of you, after reading these newsletters, often ask me about the theft that occurs at our pension fund. It is a difficult question to answer, because one person’s idea of theft is quite different than another’s. To be certain, my idea of theft is different than the City Apologists. The line between right and wrong, stealing and not stealing, corrupt or honest, has become a non-distinct, twisted, blurry line in Chicago. Generally speaking, wrong and illegal should be synonymous – when you hear “Joe Politician did something wrong” you shouldn’t have to also hear from the City Apologists when they say “Yes, but it was legal”.

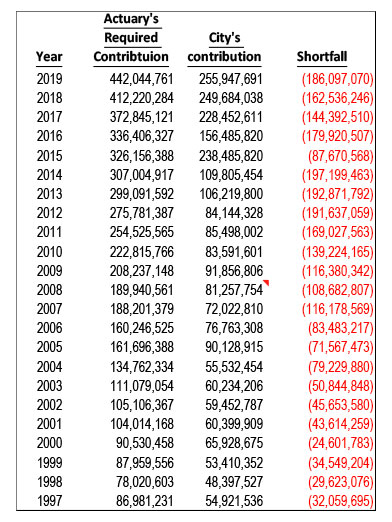

The stealing at our pension fund is no different. There exists stealing and there exists legal stealing; the stealing at our pension fund is of the legal variety. But nevertheless, we should be appalled this legal stealing is taking place at the pension fund that sustains our retirement benefits. As an example, note the table below which illustrates the amounts the professionally licensed actuaries indicate the City should put into the pension fund and the amounts the City actually puts into the pension fund. The difference is rather astounding:

For those that don’t know, actuaries are exceptionally well trained professionals that apply long standing, time tested, financial principles to the demographics at our pension fund in order to come up with the actuarially required contribution (ARC) necessary to properly sustain our pension fund. There is very little controversy about the actuarial industry or what they do. The actuaries have no conflict of interest or professional interest in inflating these contribution amounts.

The City steals from us by contributing an amount substantially less than what the actuaries calculate each year. Instead, the City contributes an amount that has been determined by the State Legislature. The State Legislature writes legislation which, contrary to the prudent application of universally accepted financial principles, allows the City to legally contribute less than what the professionally accredited actuaries determine is required to secure benefit payments to retirees in the future.

So, is this stealing? Well, I think it is. It may be legal in the Illinois political sense, but it certainly should be viewed as stealing from the perspective of firefighters and paramedics. We were promised a very clear pension benefit, guaranteed by the Illinois Constitution and spelled out in legal terms in the pension code I administer as your pension fund trustee. The mechanics of funding our pension fund to secure those benefits are clear and noncontroversial. Each year the actuaries calculate the amount the City is required to contribute in order to secure our benefits. It is very much like the salary schedule found in our contract; there is little controversy or ambiguity as to whether or not a firefighter/emt (F1B) with two years on the job should get paid $82,842 a year. It is clearly stated in the salary schedule of our contract, just like our pension benefits are clearly written in the pension code. What would Local 2 do, if instead, the City decided to pay this two year firefighter/emt $50,000 rather than $82,842? I would hope the response from Local 2 wouldn’t be – “Don’t worry about it, it will work itself out”. Unfortunately that is exactly what Local 2’s response has been, year after year, as the City has neglected to pay what is required to secure our pension benefits.

Do not make the mistake, that because the resources the City is stealing from us isn’t required to be paid until later in your career, that it is somehow acceptable. Do not buy into the morally murky logic politicians engage in as they assemble in their echo chamber, shaking hands and putting our union dues in their pockets while writing legislation that harms our families’ financial security. And more importantly, hold your labor organization accountable and speak out against the continued support of these politicians, with our union dues, who continue to pass laws that make our retirement benefits less and less secure.

I can understand members not wanting to hear that their pension benefits are at risk. And it has become common practice, especially in the news media, to discredit information that doesn’t fit a prescribed narrative by attacking the messenger. I have tried my best to hold stakeholders accountable and provide accurate information that supports my analysis; and when I make a mistake, I have no issue with admitting it, as I have done in the past. But I feel a need to respond to the attempts to discredit my analysis by attacking me personally. It isn’t so much the slanderous attacks, it is the fact that it takes the membership’s attention away from the theft of our retirement security. I can assure every member of this pension fund, regardless of what some on the Local 2 Executive Board have suggested, that I have never filed for bankruptcy nor have I ever had my CPA license revoked. I stand behind my analysis and welcome anyone that wants to question it.

I understand I am at odds with some members of the Local 2 Executive Board and it is their prerogative to vote me off of the PAC and Legislative Committee. Afterall, I clearly stated my differences with the Local 2 Executive Board as they continue to use our union dues to support the Democratic Machine in this State. But I ask the membership to again look at the table above, and maybe even again next month so you don’t forget. This legal thievery should have been this Union’s focus, not playing footsies with a bunch of yet to be prosecuted criminals down in Springfield and City Hall. The membership needs to recognize this theft, and aggressively, without hesitation, pursue the resources necessary to secure what has been promised. Stay safe brothers and sisters!

Timothy McPhillips

Pension Fund Trustee

This newsletter is my opinion only and clearly is not the opinion of the Retirement Board of the Firemen’s Annuity and Benefit Fund.

What happens when Democrats run things, they live for today and forget about the future. You hose pullers voted for them, time for you to reap what you sowed. I can't wait until they start taxing your pension at the source, so all you overpaid state and municipal employees who move out of Illinois will have to pay Illinois income tax on a pension you earned in Illinois.

ReplyDeleteGood tax the pensions! Try living on just social security.

DeleteThe pension system will fail at some point........

ReplyDeleteWhy should my tax dollars pay for your pension when I don't get a pension and have to work until I die with a 401scam It will never be enough to retire on?

ReplyDeleteIts not people stealing money from the pension it a number of things.

ReplyDeleteWhat was the actuarial's PROJECTED contribution for the future in the 1950's? Most likely it for less because the City never thought the 50 age and 20 years of duty would ever happen. But because of the 50 and 20 there are more people on the pension now than it was every funded for. This plus the reduction in mandatory retirement age forced even more people on the pension roles.

I don't like to make excuses for the City but they underfunded the pension and all the other city pension because they didn't have the money.

We used to say that the way out of this thing is to put the retirement age back to 65+ as I remember, make the current rank and file pay more and grow out of it. No more retirement until you are at least 60. It's gone to far for that solution.

I think the only solution is for the city to declare bankruptcy, let the court make all the pension regulations. Everyone takes a hair cut like United Airlines , theirs was a 50% pay cut and 50% pension reduction. A pension similar per month as the private sector.

The homeowners of this city can't afford an average property tax bill of $50,000 per year while it seems like the only people who own 2nd homes in Southwestern Michigan are City workers .

Open the pensions to all residents everyone pays in one giant fund or copy Australia's Superannuation Fund retirement system that forces everyone to contribute.

DeleteIt's not realistic for a 60 or 65 year old to do a credible job as a firefighter. Even in Chicago.

DeleteYet they were over 63 for many years.

DeleteOnce you have a heart attack, bypass or stent put in you are finished won't have the same strength physical capabilities.

DeleteThen you go on disability.

DeleteOnly two kinds of people get paid to sleep, prostitutes and firemen.

DeleteLeaked this is what we are getting retire now before you are put into this system! Hybrid Pension Plan is a market based cash balance plan and a 401(a) defined contribution plan.

ReplyDeleteCash Balance plans suck! My friend did 35yrs at FEDEX Freight only gets around $1800 month from his cash balance plan.

DeleteWhy is Union letting them get away with not making required payments for over 20yrs? We need new leadership at Local 2!

ReplyDeleteYour union leaders are in bed with the Democrat politicians and really don’t give a shit about the rank and file.

DeleteTwo things today Boys and Girls:

ReplyDelete1) If the pension is only 18% funded, then its close to becoming insolvent?

2) In some of Mc Phillips's writings I saw that he mentioned something about promotions. You know they ought to adjust the promotion scores based on how many NON EMS runs you go on. For example, if you were on Engine 45 your adjusted score would be higher than somebody with the same exam score from Engine 92. This would be because Engine 45 responds to more fires than Eng 92 where they sleep and drink beer all day.